Once you understand how insurance companies make money — and how brokers are incentivized to maintain the status quo — you stop being afraid to ask the right questions!

There is something comforting about working with the “advisors” for 15 years, as familiarity breeds trust but also complacency — and, as I recently saw, it can quickly and quietly cost your business tens of thousands of dollars. This is where Health Spending Accounts can save you from the premium ‘trap’. Let me explain.

Avoid the health premium trap

I was introduced to a company with 70 employees, spending roughly $250,000 a year on group health and dental premiums. They’d been working with the same large consulting firm for over a decade — the kind of firm that proudly touts its experience managing benefit plans for massive organizations with hundreds to thousands of employees. They had the glossy marketing decks, the oversized renewal binders, and the same pitch I’ve heard a hundred times:

“Because we work with so many groups, we get better deals and know exactly how to price your plan.”

And to be fair — that can be true. Experience and access to data do matter. But here’s what also needs to be said: just because your broker has access to all the right information doesn’t mean they are using it in your best interest.

Take control and put YOUR interests ahead of your brokers

“Just because your broker has access to all the right information doesn’t mean they are using it in your best interest.”

Most people have no idea how group insurance really works due to long-standing misrepresentation and a poor incentive model. They look at the plan summaries, maybe flip through a few pages of their renewal documents, and trust that someone, somewhere, is making sure the numbers are fair.

But the truth is, only three numbers really matter:

- Money in (your premiums)

- Money out (claims paid)

- Target Loss Ratio (TLR — how much an insurer is willing to reimburse before hiking your rates

For most small to midsize companies, the TLR sits at around 75%. That means if your team is claiming 75 cents for every dollar you give the insurer, your premiums will likely stay the same. But here’s the kicker: if your team claims less than that — say, only 50 cents on the dollar — the insurance company (like Manulife) will NOT automatically lower your premium!

They might pretend to. Maybe they offer a “no increase.” But in reality, they’re sitting on a wildly profitable group, and they know it.

I sent ONE email to save my client $50,000

In this case, my client was spending $20,000 per month. But their employees were only claiming about $12,000 to $13,000 worth of benefits. That means for every dollar the company paid, employees only got back around 60 cents. Yet the TLR for this group was only 20%. They were supposed to be getting 80 cents back, not 60.

I sent one email.

That’s it. One message to the insurer saying, “Your target loss ratio is 80%, my client’s actual claims rate is 60%, we want a discount — now.”

I backed it up with quotes from other insurers, proving those savings were real and achievable. And guess what? They got the discount. $50,000 in savings. Instantly.

Now, will this client eventually switch to a Health Spending Account (HSA)? Maybe. Maybe not. That’s their decision. But they’re now informed — and that’s what matters.

Save with a Kibono Health Spending Account

Once you understand how insurance companies make money — and how brokers are incentivized to maintain the status quo — you stop being afraid to ask the right questions.

Stop accepting renewal packages as gospel; do the math!

If your company is spending thousands every month on benefits and you’re not seeing clear, transparent reporting on claims, loss ratios, and commissions, chances are you’re leaving money on the table. And sometimes, all it takes to get it back… is one good email.

Check us out at www.kibono.ca for same-day setup

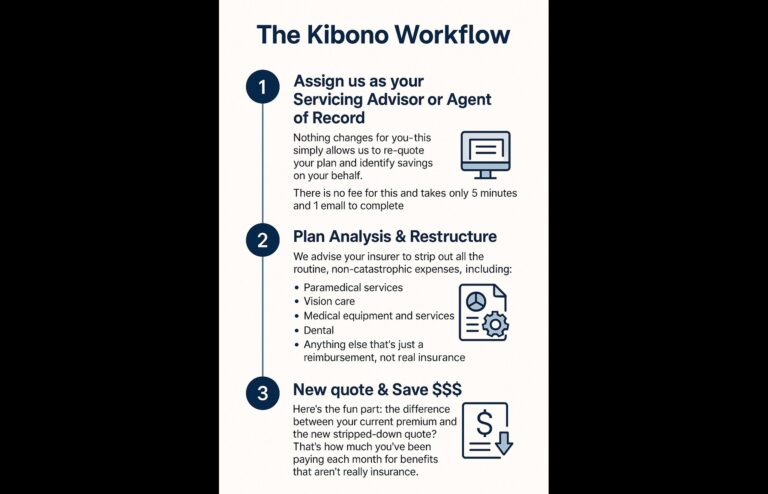

How to get started with a Kibono Health Spending Account (HSA)

- Check out www.kibono.ca for more information

- Self-Sign Up or White-Glove Onboarding at no extra charge

- Same-Day setup

- Only $2.25 + 5.25% per claim